THE last time I penned an article with the same title: “Leave conveyancing to lawyers”, it was published in the StarBiz issue on May 31, 2014. This time around, there have been calls to do away with the necessity of a lawyer in conveyancing transactions, with some naïve and uninformed layperson adopting a simplistic approach of comparing the acquisition of real property with movable property. The comparison that was given is:

“When we buy a movable luxury car, say for RM800,000, we can get our bank facility within two or three days without a lawyer. But when we buy an immovable property/condo/house for say even RM300,000, we are required to have a battery of lawyers to complete the transaction, which takes an average of three to six months.”

The Housing and Local Government Ministry is no different. Recently, it came up with the idea of an electronic form of sale and purchase agreement, acronymised “eSPA”. This eSPA module is part of the Housing Integrated Management System set up by the ministry. We will argue this “intellectual” issue in another article.

With the availability of material and resources on anything and everything, there is no shortage of professional advice. However, if you suffered from a toothache, would you seek advice from a qualified dentist or entrust the fate of your molars to unqualified quacks who have seen 100 videos on YouTube and TikTok on treating toothache? The answer is obvious; any person of sound mind would seek treatment for whatever ailments from the most appropriate professional.

Buying a car via a hire purchase contract (HP)

The pre-printed form for a hire purchase contract (HP) requires the mere clerical “filling of blanks” in the HP Schedules with description of model, make, chassis and details of the loan sum, and its monthly repayment by the hirer (customer) and the hirer’s name, address and identity.

These HPs merely require the bank officer to witness the contract and have it stamped and thereafter kept on the shelf after notifying the Road Transport Department of the ownership claim. The hirer merely has to adhere to the HP arrangement by paying the monthly instalments, otherwise risking the “repossession” of the hired vehicle. Habis cerita (case closed).

The assumption is that if you can understand legal language, you can do the lawyer’s job. Is the role of a lawyer in the sale and purchase of real property so simple that it can be equated with the same process as buying a car under hire purchase?

Signing the SPA is merely the beginning of a journey

Do you not know that the signing of the sale and purchase agreement (SPA) is merely the beginning of a journey and the tip (of the iceberg) of what entails in the sale and purchase transaction? Read on to understand better.

Why do you need to use your own lawyer? For us to answer this question, one must understand the role a lawyer plays in a sale and purchase and the reasons to engage your own lawyer.

Usually, when a vendor or purchaser decides to buy real property such as a house, apartment, condominium, shop offices, or land, they would probably consult a conveyancing lawyer. The lawyer could be recommended by the property agent or is your regular legal adviser or your relative.

We would recommend that a purchaser of real property get legal advice from the onset before committing to a purchase, and not after payment of a deposit to the vendor or the real estate agency. Reasons to seek early consultation include that the lawyer can advise you on the terms of sale and purchase; conditions of the real estate, including the implications of encumbrances over the real estate which may impede the transfer; restrictions-in-interest; and the financial commitments needed to complete the acquisition.

The Latin phrase “caveat emptor” (“buyer beware”) certainly holds true for properties. No purchaser would want to pay a deposit or the purchase price only to discover the property does not exist or cannot be purchased owing to public policy, or that the vendor is a fraudster using another person’s identity. The complications arising from a botched transaction can be severe, leading to court proceedings or financial detriment due to payment of liquidated damages. So, the role of the lawyer is not just to affix his/her signature; it is to protect the interest of a vendor and purchaser and to act as a filter against any irregularities in dealings.

We know of property agents who propagate the belief that both purchaser and vendor can “share” a common lawyer so that there are some savings in legal fees. That is an untrue proposition and puts the vendor at a disadvantageous position. In the sale and purchase of property, lawyers cannot represent both a vendor and purchaser. If a vendor chooses not to appoint a lawyer, the vendor is considered not legally represented.

In general, most real property transactions undertaken with lawyers on board do tend to complete successfully because the lawyers are able to navigate the technical and procedural complexities associated with land and tax laws. The benefits of having legal advice and a problem-free transaction outweigh the fees payable for legal services. The adage “Don’t be penny wise, pound foolish” is most appropriate.

There are some differences in buying a property from a developer or from an individual or company that already owns the property, which we term as a “sub-sale”, short for subsequent sale. In this article, we would concentrate on the purchase of a residential property from a licensed housing developer.

Purchasing from a licensed housing developer

The purchase of residential property from a housing developer is regulated under the Housing Development (Control and Licensing) Act 1966, which has been amended from time to time to keep up with ever changing face(s) of residential development. Pursuant to HD Regulation 11(4), the purchaser lawyers shall be entitled to a complete set of the SPA, including all annexures “free of charge” from the developers, subjected to the lawyers’ undertaking etc.

From a purchaser’s perspective, buying from a developer is even more simplified: they choose a unit, apply and obtain the loan, sign the SPA, pay the deposit and wait for the property to be completed. On paper it sounds easy enough. However, the actual process for completing the sale and purchase is not a mere three-step process, contrary to popular belief. The end goal of any sale and purchase is to ensure that the property is properly conveyed to the purchaser. The process of conveyance has grown more complex; transferring a property from one to another has evolved through the years to ensure that the right property is transferred to the right persons and to prevent fraudulent transfers.

Most of the essential work done by the lawyer is not known to the parties in a sale and purchase transaction. As far as the purchaser is concerned, once they pay the legal fees they expect (rightly so) the lawyers to complete the legal process, so that the housing loan will be available for release progressively to the property developer, and to wait for the end of the completion period, usually 3 months, and thereafter to take delivery of vacant possession of the real property. To a vendor, it may look even simpler: sign the SPA and wait for the payment. If you are buying directly from a developer, the time for you to get the property varies from 24 to 36 months onwards depending on the type, unless the real property is almost or already completed.

Preliminary verification exercise in SPA transaction

Before one even signs a SPA, some preliminary matters need to be addressed, such as whether the developer has obtained the proper and upfront licences and requisite approvals from the government and related agencies; confirmation of the unit being purchased; the type of property being purchased; the approved layout plans of the property; what essential items come with the property; the schedule of payments; the relevant identification documents of the developer and purchaser; and conduct the relevant bankruptcy, winding up and land title search.

If all these are in order then the SPA can be signed by the parties. The duly signed SPA will now proceed to stamping of the contract at the stamp office.

Stamping is done online, and the stamp office issues a stamp certificate to show duty has been paid.

Stamping of the SPA does not convey ownership to a purchaser. At this point, for those purchasers that have taken a loan to part finance purchase the property, the financier’s lawyer will have to coordinate with the solicitor in charge of the SPA to prepare the loan facilities documentation.

Memorandum of transfer

Do you not know that pursuant to Section 211 (Fifth Schedule) of the National Land Code 1965, the designated persons to attest or witness the signatures appearing in all dealing instruments including, but not limited to MoT are “an advocate and solicitor (a.k.a. lawyer)” and a host of others permitted by the legislation? The bank officers/commissioner of oaths/clerks cannot attest/witness the signatories to the memorandum or such dealing instruments.

Undertakings and performance in housing loan transaction

The loan documentation is a tedious and complex process with every bank having their own drawdown requirements and processes. Each party or parties instrumental to the transaction has to issue their respective confirmations and undertakings; be it the SPA lawyers, housing loan lawyers, the property developer and the bank financiers. Hence, the time required for effectual disbursement of the loan (or part thereof) would consume approximately 3 months, to be conservative, depending on its complexity.

End-to-end conveyancing process in immovable property transactions

The following is the checklist (which varies from banks to banks having different pre-disbursement criteria) that conveyancing lawyers have to perform and undertake to the purchaser’s banks/financier, though not exhaustive, inter alia:

Land searches to ascertain the land information as represented in the SPA is correct and to confirm the presence or absence of any encumbrances, restrictions, prohibitions, or acquisitions on the land in which the buildings are erected, which may materially prejudice a financier’s interest or cause the financier to not be able to register their interest over the purchaser/borrower’s housing unit or parcel.

Searches on the developer, vendor (for sub-sale), purchasers/borrower to establish their solvency. If the purchaser/borrower is a company, there are additional checklists such as reviewing the Board of Directors resolutions and ensuring the corporate documents are in order.

For properties which are still under a master title, the end-financier lawyer must obtain letters of undertaking from the developer to assure the financier that the developer will effect the transfer of the property to the purchaser once the separate strata title is issued; not to encumber the land any further through the creation of additional charges; and to apply for consent to transfer and charge. The financier lawyers also write to the purchaser’s lawyer to seek their undertaking to attend to the perfection of the transfer once the separate strata title is issued. The responses and documents requested are then subsequently reviewed to ensure the contents comply with a financier’s requirement and, if need be, the financier lawyers will seek further information or clarification from the developer. If the master titles are charged to a financial institution (bridging financier), the end-financier lawyer will also need to request for a redemption statement and a letter of disclaimer, whereby the master charge agrees not to foreclose the purchaser/borrower’s unit or parcel so long as the redemption sum is paid.

The above do not include other checking, such as sighting of the developer’s licences; approvals for the project; issuance of the certificate of completion and compliance (for completed projects); and ensuring the quit rent and assessment have been duly paid to the land authorities and local council, respectively. Not all loan processes are standard as development projects may have different schemes as a leaseback arrangement or guaranteed income scheme, in which a lawyer would also need to advise a financier on the terms of the scheme and its impact on the financier’s interest in the property.

Then, there is the procedure to witness the instruments, endorsement, affirmation of the Statutory Declaration, stamping process, registration and extraction thereof.

The Letter of Advice for release of loan which is issued by a lawyer/law firm to the financier is not a mere one pager; it usually runs to pages and pages (some nearly nine pages) of confirmation of facts; that information and certain actions have been taken, such as lodgment of caveats to protect a financier’s interests; explanation on the land conditions; applicable public policy for special housing schemes; compliance by the relevant parties to the conditions set in the financier’s letter of offer; and that the loan and security documentation has been properly executed, affirmed, stamped and registered, where required.

Once the drawdown requirements are satisfied, the financier lawyer then advises the financier to release part of the loan sum to the master charge (bridging financiers) for redemption purposes and thereafter to the developer’s Housing Development (Project) Account when the developer issues its progress claims to the end-financier and purchaser.

The letter of advice may be uploaded onto a financier’s portal or printed in hard copies. The letter from the lawyer/law firm entrusted with the housing loan usually contains a professional undertaking from the lawyer/law firm to the financier to make good on any loss or damage suffered by a financier for any negligence, error, omission or mistakes.

It is not such a simple and straightforward process as perceived.

The end to end conveyancing process list is non-exhaustive.

Discounted legal fees

We do acknowledge that the amount of work that has to be done should be, and is, taken into account in the scaled fees.

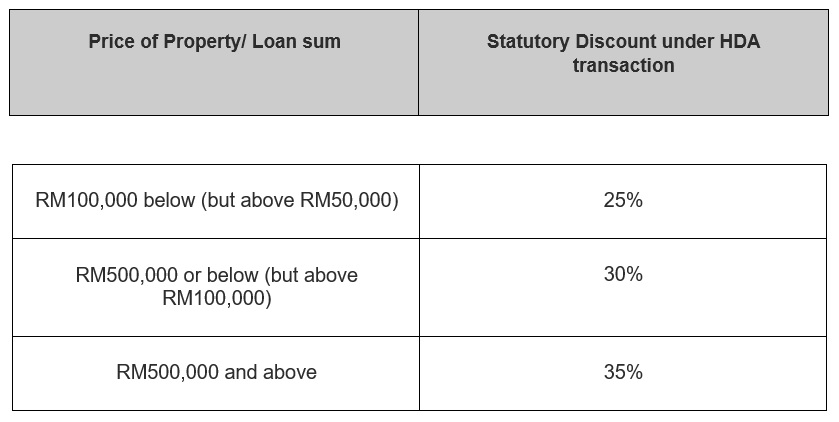

However, in a case where the purchase transaction is governed by the Housing Development (Control and Licensing) Act 1966 (HDA transaction), or where a loan is obtained to finance a HDA transaction, a permitted lower scale of fees will apply, ranging from 25% to 35% discounts (TABLE 2) based on the Solicitors’ Remuneration Order 2005, which was gazetted on March 2, 2017 and came into operation on March 15, 2017.

The legal fees are calculated based on a percentage of the buying price of the property or housing loan sum, which can be anywhere from 0.5% to 1% (TABLE 1) :

Such discounted legal fees are certainly to the benefit of purchasers. Regardless that the said SPA is in statutory form, professional insurance still has to be purchased by lawyers to cover all circumstances.

To our mind, the scaled fees work better for the lower-income group.

Without the scaled fees, I think lawyers will likely charge more for lower-end properties because the amount of work involved is often the same as higher-end properties.

In the case of purchase of a low-cost house, it entails having to apply for the formal consent of the state authorities, land office and sometimes the local council on top of having to recite the status of the property in the sale and purchase contract – that’s more tedious work than a higher-end freehold property.

With the compulsory discount, I do not think house purchasers for low and medium-cost houses are overcharged.

Conclusion

Now, what else have I omitted to argue the case of requiring professional legal services in conveyancing? The task entails voluminous work and only a “hands-on” legal practitioner aka lawyer would understand the intricacies of the processes.

Of course, academicians understand the peripheral procedures but they are not “practising” per se, and merely lecture on the ideal.

What more a nescient layperson who doesn’t have full knowledge of the legal intricacies, process, obligations, and possible liabilities. – The Vibes, May 17, 2022

Datuk Chang Kim Loong is the honorary secretary-general of the National House Buyers Association (HBA), which can be reached at [email protected]

This article is intended to offer an insight into the works of the conveyancing processes vis-à-vis sale and purchase and housing loan transactions. If in doubt please seek your own independent legal advice