THERE should not be any doubt that Malaysia is currently facing a housing crisis where the majority of the rakyat cannot afford to buy their first home.

As early as 2012, the National House Buyers’ Association (HBA) had warned that housing prices were beginning to escalate out of control and, unless immediate remedial measures were taken, a “homeless generation” will emerge where an entire generation or even generations of the rakyat, from the lower- to middle-income segment and fresh graduates will not be able to buy their first homes.

To quote from Bank Negara Malaysia’s (BNM) 2016 Annual Report: “Since 2012, the increase in house prices in Malaysia has outstripped the rise in income levels. Consequently, prevailing median house prices are beyond the reach of most Malaysians.”

The situation has not improved in 2022. Based on BNM’s Financial Stability Review Report Second Half 2021, the median property price in Malaysia is 4.7 times the median income in the country and can be classified as “seriously unaffordable” by international standards.

Fixing the current housing crisis is not going to be easy or fast as the crisis did not just happen overnight. Various parties have come out with their own formulae or suggestions on how to enable the rakyat to buy their dream homes.

HBA perspective on intergenerational loans

There are various permutations on what intergenerational loans – also known as second generation loans or dual generation loans – mean, but in a nutshell, these housing loans entail one or more of the following features:

(i) Borrower taking a housing loan with tenure of 40 years or more which will well exceed their expected retirement age.

(ii) Borrower has an option to make a bullet repayment to fully repay the outstanding loan amount using their Employees’ Provident Fund (EPF) savings upon reaching retirement age.

(iii) When the borrower is no longer able to work and if the housing loan remains outstanding, the borrower’s children, i.e. the second generation can continue paying for this housing loan until it is fully settled.

While the government may have good intentions for every rakyat to own a home and for families to live together, the HBA believes that intergenerational loans or second generational loans or dual generation loans (referred collectively to as “intergenerational loans”) will not help to solve the current housing crisis and will only exacerbate the situation in the mid- to long-term. The HBA believes that the government may have been ill-advised by parties with vested interest, namely financial institutions and housing developers on the merits of these so-called intergenerational loans.

First generation unable to retire comfortably

The main reason why most house buyers buy a house is so that when they retire or stop working, they will have a roof over their heads and not be homeless. Else, why bother going through the hassle when you can just rent a house? Hence, it is important that house buyers match the liability of owning a house against their expected income stream.

A mismatch can result in house buyers being unable to service their mortgage obligations and risk foreclosure by the financial institutions, which can result in property bubbles and even global financial crisis, as evident from the sub-prime crisis in the United States which resulted in the worst economic crisis since the Great Depression of the 1930s.

By taking these intergenerational loans which carry a loan tenure 40 years or more and which will extend to at least 70 years of age – assuming the borrower was just at a relatively young age of 30-years-old when the loan was first taken – the house buyer may not be in a position to retire or stop work when they reach 60-years-old and must continue working to service the outstanding loan obligations in the event for whatever reason, the second generation is unable or unwilling to serve the remaining outstanding obligation.

What if the house buyer is no longer in optimum health and can no longer work? Under this scenario, they will face foreclosure even after paying the bank loan for more than 30 years.

EPF savings are meant for retirement

As mentioned, some intergenerational loans might have the feature of a bullet repayment of using the EPF savings upon the borrower reaching their retirement age to fully repay the loan.

However, in reality, the majority of Malaysians do not have enough money in their EPF to retire comfortably and hence will not be able to use their EPF funds to repay the balance of the intergenerational loans upon retirement.

It has been reported that EPF estimates that 73% of its members will not be able to meet the already low basic savings threshold of RM240,000 at age 55 to retire and some 46% of its contributors below 55 have less than RM10,000 in their EPF accounts.

The primary reason for the EPF is so that contributors will have some financial safety net upon reaching retirement age. Even for those who may have excess funds in their EPF account, exhausting the EPF savings to fully repay the intergenerational loan is not a good move as it would mean that the borrower would not die homeless but possibly die of starvation.

Higher interest expenses

It cannot be denied that the monthly instalments for these intergenerational loans are lower than a conventional loan tenure but because the tenures are significantly longer, the house buyer also pays significantly much more in interest expenses over the entire tenure of the housing loan.

In some instances, the interest portion can even be higher than the principal loan amount.

The HBA recommends that house buyers should ideally take loan tenures of 20 years and if necessary to stretch it up to 30 years – but never beyond 30 years. If you cannot afford it over 30 years, accept reality and buy something more affordable.

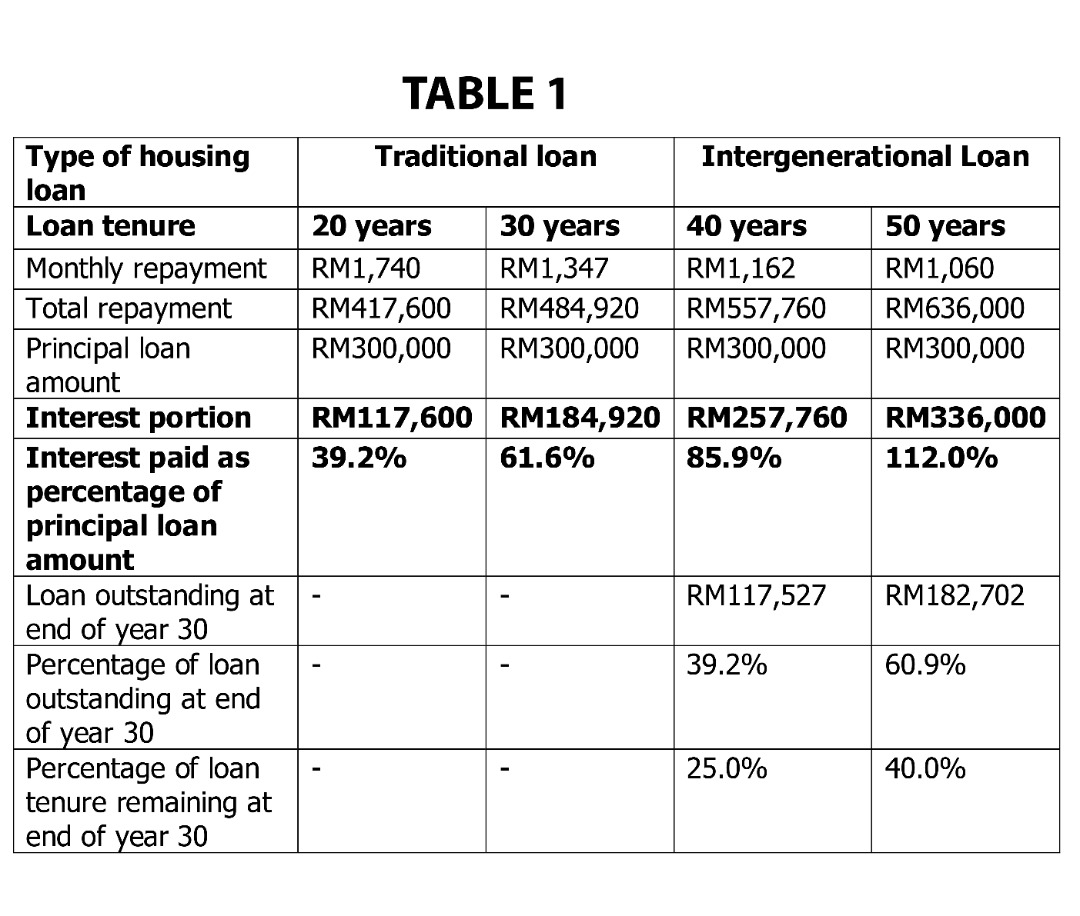

To illustrate, based on a housing loan of RM300,000 and assuming an effective interest rate of 3.5% p.a. over the entire tenure, the monthly loan repayments of a 20-year to 50-year housing loan is as follows:

As illustrated above, no doubt it appears that the monthly repayments for an intergenerational loan are lower than traditional loan tenure (approximately RM578 lower comparing 20-years and 40-years loan tenure) but in reality, it means that the house buyer saves RM578 for the first 20 years but ends up paying RM1,162 extra for the next 20 years.

By taking an intergenerational loan and stretching the loan repayment tenures longer, the interest portion for an intergenerational loan can be higher than the principal amount of the original loan. Hence, it is more economically beneficial to the house buyer to take shorter loan tenures and pay off the housing loan faster.

Better a pain while the house buyer is still gainfully employed.

Loan outstanding is not directly proportionate to tenure outstanding

Current practice: The monthly loan instalment that the borrower pays to the bank is split between paying the interest and the balance will then be used to reduce the principal loan amount.

As the principal loan outstanding is high at the start of the loan, a higher amount of the monthly loan instalment is used to service the interest.

Hence, the principal loan outstanding does not correspond directly to the remaining loan tenure.

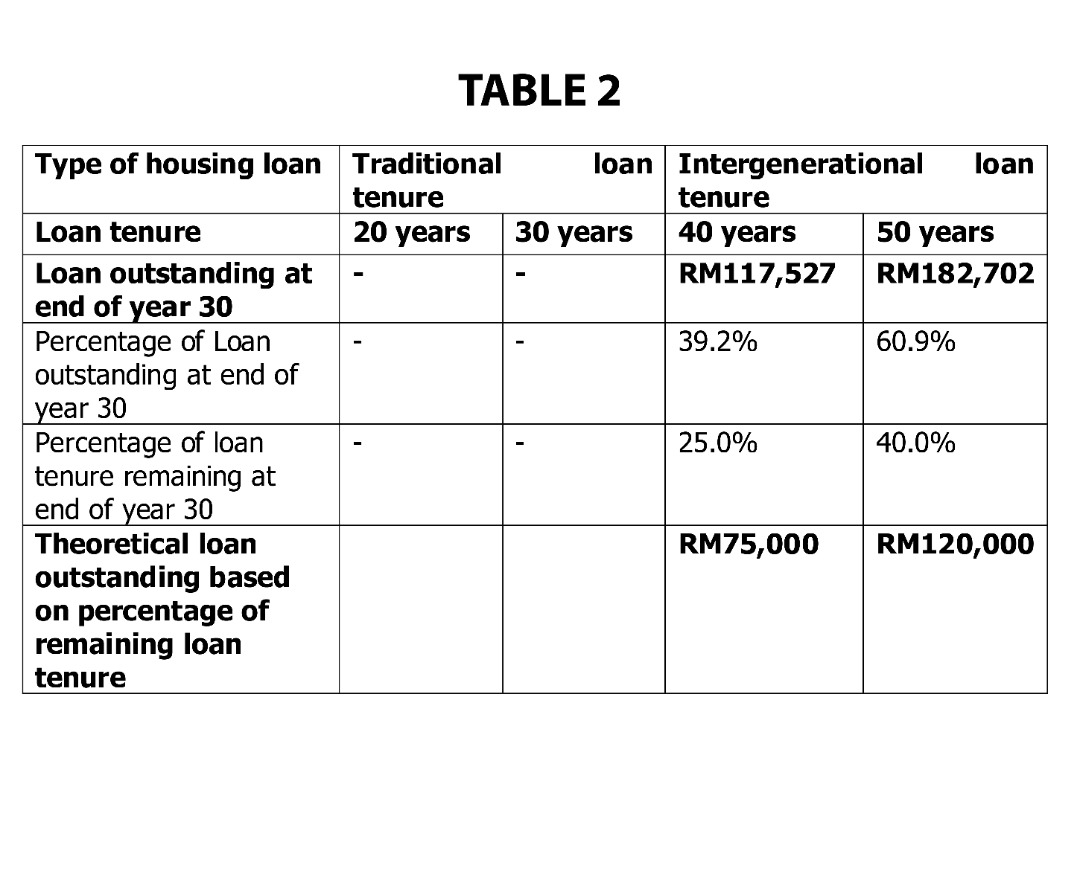

Referring to Table 2 below, if the borrower takes an intergenerational loan of say 40 years and has paid 30 years or about 75% of the tenure; the borrower may expect that since they have paid 75% of the tenure, the loan outstanding would be 25% of RM300,000 or RM75,000. However, in reality, the loan amount is RM117,527 or 39.2% of the original loan amount of RM300,000. If the borrower had taken an intergenerational loan tenure of 50 years, the borrower would have paid 60% of the loan tenure, the loan outstanding is RM182,702 or 60.9% of the original loan amount.

The borrower would have underestimated the actual loan amount and could be out of the money in trying to settle the loan outstanding and could be forced to either continue working or to get their children to take over the remaining loan obligations or risk the banks foreclosing on the property after diligently servicing the loan obligations for 30 years.

Second generation born into ‘debt’ or ‘slaving for the bank’

In the olden days when slavery was legalised, children of slaves were born into slavery. Slaves had no rights and neither did their children and this cycle perpetuated itself. By taking an intergenerational loan, these house buyers would have inadvertently committed their children to a financial commitment even before their children are old enough to enter into any sort of legal contract. Parents should only bequeath inheritance to their children after their own passing and never leave them with unpaid financial commitments. What if there is a situation of several children (born and unborn at the time of the loan)? What about division of property (civil or shariah) in the event of the demise of the principal borrower? Which one of the children should “inherit” the burden?

Hence, when their children are just entering the workforce, the second generation have a financial commitment and a burden to serve that they did not enter into and cannot be broken without jeopardising their parents – whom could be sued by financial institutions for non-performance or risk the family home being foreclosed. Is it fair to the second generation to face such financial commitments? What if their children have to work in other states and have their own family?

Would they be able to service their own financial obligations and this intergenerational loan at the same time?

Only suitable for short-term buyers, speculators

So, given all the disadvantages surrounding intergenerational loans, who then would apply for such loans? In the HBA’s opinion, such intergenerational loans would only attract house buyers cum investors who wish to live in the said property on a short- to medium-term basis (say 3 to 5 years) and want to hedge against any potential increase in rental rates (or sudden eviction by the house owner) and/or property speculators who wish to make a quick buck and lower their costs. Table 3 illustrates such a scenario.

Using the same information in Table 1, short-term house owners cum investors or property speculators are better off if they take intergenerational loan tenures of 40 years or longer and only stay/hold for about 3 to 5 years before selling off the said property and moving on to another one.

This is because the equivalent rental yield paid by such house owners/investors/ speculators may be even lower compared to renting outright or a conventional loan tenure. Besides, such short-term owners are able to freely renovate their property as they wish for something that they cannot do if they just rent.

However, such short-term house buyers cum investors or speculators are subject to risk of the property prices fluctuating.

Chief beneficiaries are financial institutions, housing developers

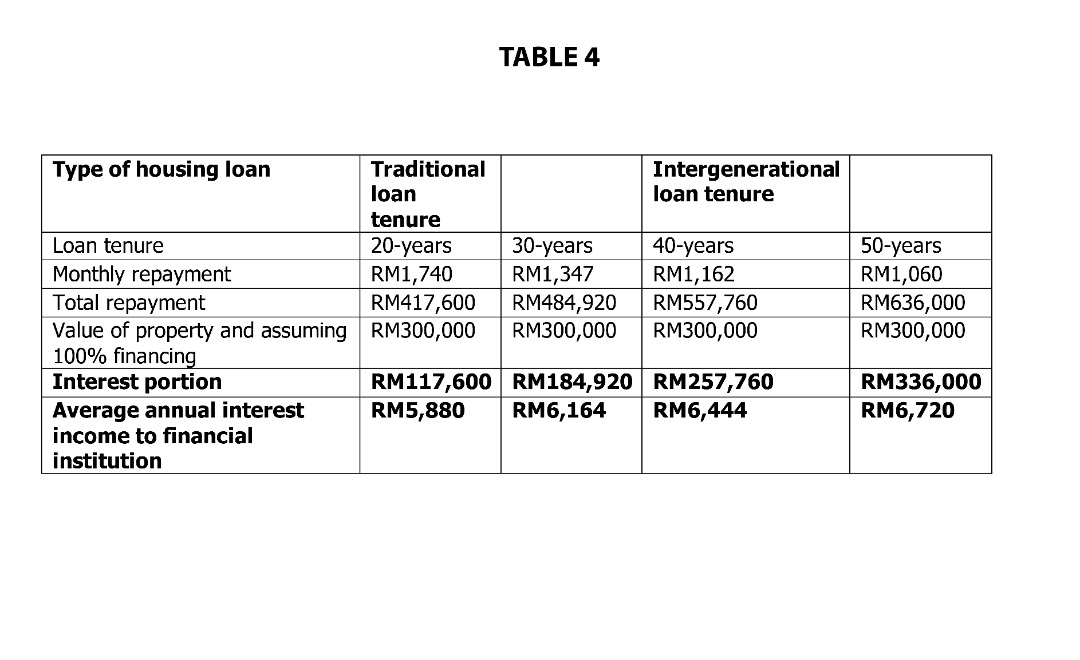

The chief beneficiaries of intergenerational loans are financial institutions and housing developers. Financial institutions will make a higher profit as evident from Table 4 below and housing developers will be able to sell properties of higher value because financial institutions are willing to finance such properties. This will only worsen the situation where the younger generation are not able to buy their first homes.

Government must give incentives for affordable housing

The current government must continue with its aspiration for every rakyat to have a roof over their head, but intergenerational loans or second generation loans are not the answer. The government should take cognizance of the fact that intergenerational loans or second generation loans can be abused by property speculators as a means of cheap financing and disallow financial institutions from extending such loans, which will only worsen the housing crisis in the mid- to long-term.

The current government should offer incentives for housing developers to build affordable housing for the masses, especially the lower- and middle-income group.

The government must also put in place measures to stem excessive property speculation fueled by easy credit, such as imposing higher stamp duty for transfer of properties and higher real property gains tax for owners of multiple properties. – The Vibes, December 10, 2022

Datuk Chang Kim Loong is honorary secretary-general of the National House Buyers’ Association, which can be reached at [email protected]