By Murray Hunter

MALAYSIA’S economy continues to post respectable GDP growth figures, yet beneath the surface lies a deepening structural crisis that official statistics barely acknowledge.

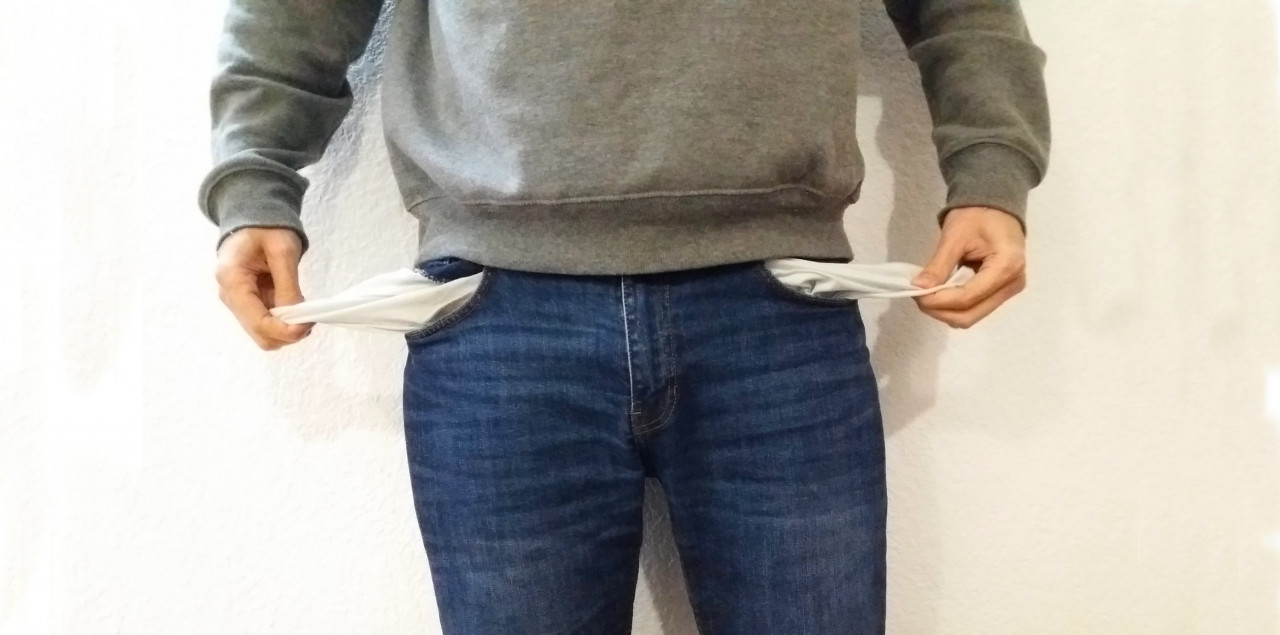

Household debt has climbed relentlessly over the decades, now sitting at around 84–85 per cent of GDP as of mid-2025, placing the country perilously close to Thailand’s regional high of roughly 87 per cent.

What began as access to housing and vehicle financing has morphed into something more insidious: a debt culture that is quietly reshaping family survival, business viability, and national resilience.

This is not mere leverage. It is a form of invisible poverty.

From roughly 40–60 per cent of GDP in the early 2000s, household borrowing has ballooned on the back of aggressive property and motor vehicle financing, which still dominate portfolios.

For many families, up to 50 per cent or more of their monthly income now services home loans and car repayments alone.

That leaves precious little for essentials like schooling, food, healthcare, or simple emergencies.

When wages remain largely stagnant in real terms, especially in the private sector and informal economy, the arithmetic becomes cruel.

Families borrow to maintain appearances of middle-class life, only to sink deeper into the trap.

This debt burden now exerts more influence over family planning and daily survival than almost any other factor. Young couples delay marriage or children because of loan commitments.

Parents forgo quality education for their kids to keep up with bank instalments. Retirement dreams evaporate as CPF-like savings are raided or never accumulate.

It is a slow erosion of aspiration, masked by shiny shopping malls and glossy economic reports.

The problem extends into the backbone of the economy.

Micro, small, and medium enterprises (MSMEs) are being hit hard due to a lack of financing capital.

Many lack access to proper business financing channels and instead rely on personal or consumer credit cards and personal loans.

The high interest rates on these facilities drain cash flow, hobble investment in growth, and contribute to poor performance or outright failure.

This is not entrepreneurship; it is survival borrowing that perpetuates low productivity and stifles genuine innovation.

The irony hangs heavy as the primary providers of this household credit are largely government-linked companies (GLCs) and banks under significant state influence.

These institutions report bumper profits year after year, distributing dividends that help fund government budgets and patronage networks, while ordinary households shoulder the repayment risk.

The same entities that dominate the economy through preferential access and regulatory shields are effectively extracting rent from citizens’ future income.

Public discussion of this crisis remains muted.

Mainstream narratives prefer to highlight “manageable” debt service ratios and prudent lending standards.

Bank Negara Malaysia offers reassuring assessments, yet vulnerabilities are clear among lower-income (B40) and even squeezed middle-income households.

Official poverty figures fail to capture this leveraged precarity because families who are asset-rich on paper but cash-poor and one shock away from default.

This is structural poverty disguised as financial inclusion.

The deeper malaise ties into broader patterns of stagnation.

With limited real wage growth, a segmented labour market heavy on foreign workers in lower tiers, and productivity gains captured disproportionately by capital and connected elites, households turn to debt to bridge the gap.

GLC dominance, remnants of policies originally designed for redistribution, now often channel resources away from broad-based opportunity.

Education systems and regulatory burdens compound the issue, leaving too many Malaysians in low-value cycles.

Malaysia risks normalising a dangerous equilibrium.

A high GDP aggregates alongside the lived experiences of financial stress for households.

Without targeted relief such as meaningful debt restructuring support, wage-productivity linkages, easier SME financing, and reforms to reduce reliance on high-interest consumer credit, this quiet crisis will fester.

It already shapes demographic decisions, entrepreneurial dynamism, and social cohesion more than policymakers admit.

Debt has become a major cultural aspect in Malaysia.

It funds the cars in driveways, the roofs overhead, and increasingly, the illusion of progress itself.

The question is whether the nation confronts this leveraged reality before it constrains future generations, or whether the providers of credit continue to thrive while families tread water.

The window for honest policy intervention is narrowing, as it always does when uncomfortable truths sit below the radar. – June 25, 2026

.jpeg)